Making Sense of Investing

Here’s a deep-dive into investing, articulated and contributed by Shrishti Sahu, a leap.club member…

Here’s a deep-dive into investing, articulated and contributed by Shrishti Sahu, a leap.club member.

____________________________________________

Investing is a beautiful journey that teaches you about patience and wealth creation. Why should you invest? One simple reason: Wealth cannot be earned, it can only be created. Regardless of the sum, you start with, 20–30 years later you can end up with a significant corpus that will help you live a financially independent life. Why should you aim to live a financially independent life? Another simple answer: regardless of gender, who you’re married to, who your parents are & what you may inherit or earn — personal money management is a critical life-skill that gives you the freedom to live life on your own terms.

Goals

Each person has their own unique goals and their own perspective when it comes to ‘money’. Your goals are personal and need to make sense to you (and no one else). Start by defining what matters to you, why & what can help you get there. You could categorize your goals as achievable, stretch and dream goals, and/or you could classify them as monthly and annually. Some examples:

Use X% of my salary/income towards investments

Put $Y towards a vacation fund

Put $Z towards children’s expenses

Set aside $A for monthly ‘experience’ spend (could include eating out, shopping, and other lifestyle expenses)

Increase my net worth by $B

Contribute $C towards the retirement fund

These goals should be monitored regularly, and adapted to your life’s changes or even changes in goals themselves. For example, you may decide that you don’t actually want a Ferrari, you’d rather get yourself an Audi and use the extra money towards your child’s education and that would be a fair trade-off. Most people start with audacious goals like ‘I want to buy an island’, ‘I want to buy a Rolls Royce’ or something on those lines without realizing how these goals may be enforced by you by the society. However, for goal-setting, each goal should help you get closer to the life you actually want, be long-term (nothing worth having comes easy), and realistic. While not arguing the fact that you can earn your way to a Ferrari — but is it something you really want is an important first step. To become a successful investor, you really need to become self-aware & that’s true for anything you do in life.

Maintain your own P&L a.k.a Budgeting

If you’ve ever run a business, you may understand the art of budgeting. If you haven’t then it’s a good time to learn. What’s a budget? “A plan of how to spend an amount of money over a particular period of time to achieve the goals you set.” While doing this for a business is extremely helpful, we almost never apply it to our own personal lives. Once you put together your list of goals & your budget — your path to getting closer to your dreams will be clearer to you & may also change the way you operate in life overall. For example, instead of spending a certain amount on shopping in a certain month, you may consciously start allocating it to your retirement fund because you don’t want to work well in your 60s and just making a small change in your spending amount right now will compound over the years.

When thinking about how to set goals & budget, you need to:

Take stock of your current situation (income, savings, investments, assets, liabilities — spell it all out on an excel sheet)

Define your goals & where do you want to reach (buy a home, children’s education and weddings (used to be the top-most goal for most Indian families) which is changing with millennials today, holiday home, vacation fund, retirement fund, net worth goal)

What do I already have to get started?

What’ll get in the way or blockers?

Who are the key people to reach out to when I need help?

Net worth = Assets (what you own) — Liabilities (what you owe)

Living a debt-free life is underrated. Most people spend beyond their means to achieve status quo but always keep in mind that debt actually eats at your net worth.

Maintain an expense tracker (eating out, groceries, rent, car/fuel, travel, insurance, whatever is a cost bucket in your life). Set a budget for yourself & stick to it. Maintain an income tracker (salary, rental income, dividends, bonuses, gifts — everything that gets cash in etc) and try to introduce new revenue streams for yourself when you can.

Just by taking stock of my expenses, I was actually able to decide the areas I wanted to cut down my spend on — for example, do I really need to eat out every meal on the weekend (a significant portion of my monthly $ was going towards dining out (close to 15% some months! & I had no idea! Do I really want to buy this dress or would I rather put it towards my vacation fund? We are all making these choices unconsciously anyway — maintaining trackers brings it to life & helps you see the trade-offs IRL.

Saving & emergency funds

Set a goal for yourself — say 20% of your income every month should get invested. This % only needs to make sense to you, but shift your focus from ‘saving after spending’ to ‘investing before spending’. If you really want to see your net worth grow, the goal should be to keep moving higher in terms of absolute percentage of total income. With the number of options available today of fintech apps, it’s a good idea to automate investments on a monthly basis.

Contribute 6–9 months of monthly spend towards an emergency fund AND don’t touch it, no matter what, unless of course an emergency! The budgeting exercise that we covered before should give you a ball-park figure of your monthly expenses, so build your emergency fund accordingly.

Spending & Expenses

In the book Psychology of Money, Morgan Housel talks about how people spend much more than they have, take on debt to appease and conform to ‘society’. The only signal you get from someone’s luxury spend is ‘the money they spent’ not the ‘money they have’. If you admire someone’s ‘rich’ or ‘instagrammable’ lifestyle, you may fall into the trap of admiring someone who may be living on the edge and way beyond their means or overall are just awful at personal finance. Getting rich is very different from staying rich. We have all heard of billionaires who couldn’t sustain their expensive lifestyles. Money exaggerates the person you already are. So if you can become good at personal money management when you don’t have a lot, this habit will serve you well in the long run. While we can all sit back and wish for $10MM in our bank accounts, there really isn’t any get-rich-quick scheme that can get you there. A lot of wealth that you see accumulated, has been because of people who set out to do it long term.

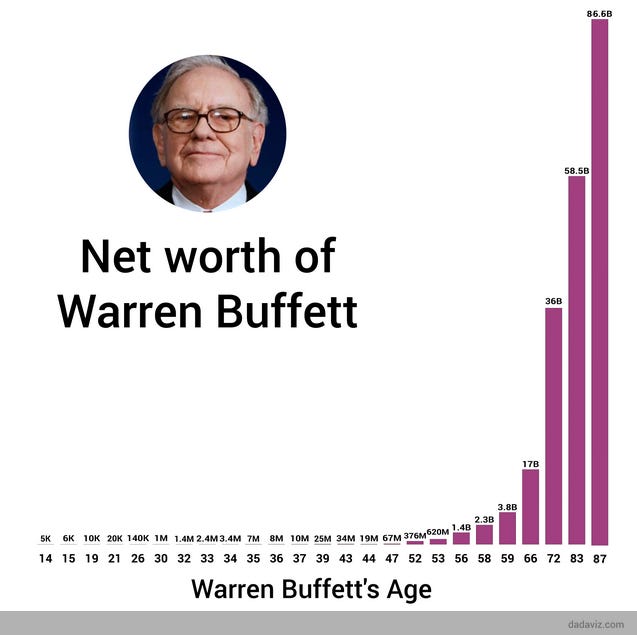

Warren Buffet in fact made 95% of his wealth after he turned 60. While today’s social media makes people project spend-heavy lifestyles, accumulating true wealth is actually a long-term, slow, and even boring game — that works on centuries-old principles. Don’t fall for instant gratification, it hurts your long-term net-worth goal. And to those who say YOLO & would rather spend it all than invest — good luck, let me know how that works out for you!

Portfolio creation

When you think about creating a portfolio, you must remember that diversification is key. There are many asset classes available: equities, debt, real estate, gold, cryptocurrencies, startups commodities etc but you need to do what makes sense for you and works for your risk profile. It’s true that you can double your money every 3 years if you strive for 24% IRR annually. 10L compounded and grown at 24% every year, in 30 years can be close to INR 100 Crores (yes, that’s the beauty of compounding..10–20–40–80–160–320–640–1280–2560–5120–10240) — which is a serious sum of money for anyone. And 24% in equities is pretty achievable but it also requires a lot of homework and due diligence to actually know the businesses you’re buying into. For anyone who’s not willing to spend time to study the markets, trends, companies the safest bet is actually index funds (12–14% CAGR) which also happens to be the lowest risk, modest reward & can be done via the SIP route consistently over the years. In fact, Warren Buffet too, has always maintained that instead of giving your money to money managers on Wall Street, just consistently invest in index funds, and some decades later you’ll actually end up with more money than people who may invest in equities without knowing what they’re getting into. Most mutual funds unlike their tag line ‘mutual funds sahi hai’, are actually not great investments for common investors because they’re optimized for paying the fund managers (fund managers earn a commission on how much money they’re managing AKA AUM VS the profits they make; thus unaligned incentives hurt the performance of the industry & returns of common investors at large). Real estate, while great to have, also happens to be illiquid (selling properties takes months if not years) and is delivering less than 5–6% returns IRR considering how long people end up holding the assets before selling. Fixed-income assets such as FDs (all our parents’ fav investments) barely give you 1% returns (when adjusted for 4–5% of inflation year-on-year) at 6–7% (or lower these days). Cryptocurrencies, startups, and commodities are absolutely a no-go for new investors because they’re in the highest risk category and most of the investments should be seen as write-offs rather than assets. Lastly, the Indian favourite of all time — Gold! This asset-class is already in most Indian portfolios and should stay because it has historically been a safe bet & delivered good returns over the long-term (~8%).

Given these facts & your personal goals, decide the allocation depending on what your goal IRR per year is & that is how you should construct your portfolio.

Power of compounding

Compounding can apply to areas beyond investing — it’s one of my guiding principles in life when thinking about personal development, health, learning, relationships, and more. For each area, a small input can lead to large output, and the results build upon themselves. Most people think that investing is Warren Buffet’s skill but ignore his secret sauce: time. He started investing at 10 and is still investing way into at 90. That’s 8 decades of compounding working in his favour. No matter where you start, 1L, 10L, or 1Cr — compounding is the magical instrument that will help you achieve a serious amount of money — and the only thing you need to do is be patient & let ‘time’ work its magic.

If you enjoyed reading this piece and would like to continue receiving non-BS tips on personal finance and investing — please subscribe to her weekly newsletter here sahu.substack.com.